Geopolitical Shocks Test Thailand’s Mid-Market as Confidence Softens Further in Q1 2026

The outbreak of war in Iran has added a further layer of pressure to an already challenging operating environment for Thailand’s mid-market as the country enters 2026. The conflict compounds longstanding domestic and structural challenges that continue to differentiate Thailand from several of its more resilient ASEAN peers.

According to Grant Thornton’s latest International Business Report (IBR) for Q1 2026, only 19% of Thai business leaders express strong confidence in economic improvement, down sharply from 31% in the prior quarter. While the regional backdrop remains mixed, the gap between Thailand and its neighbours is becoming increasingly difficult to ignore as uncertainty, slower decision-making and tighter cost controls take hold across the market.

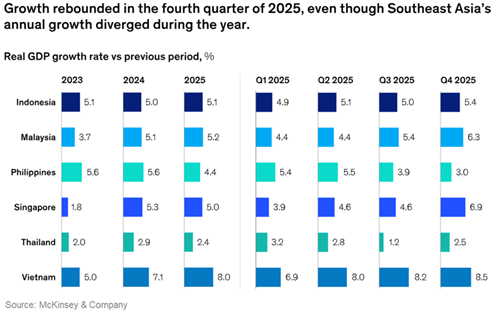

Southeast Asia’s Growth Diverges in 2025, But Ends the Year on a Stronger Note

Southeast Asia closed 2025 on a stronger note overall, with growth accelerating across most economies in Q4. Vietnam reaffirmed its position as the region’s standout performer, lifting full-year growth to 8.0%;its highest rate since 2011. Malaysia surged to 6.3% in Q4, Singapore reached 6.9%, and Indonesia recorded its fastest growth in over two years at 5.4%.

Thailand also recovered from its weakest quarter since 2021, rebounding from 1.2% in Q3 to 2.5% in Q4, with all sectors posting growth for the first time that year. However, full-year expansion of just 2.4% left Thailand trailing every other major economy in the region, underscoring the scale of the competitiveness gap and the structural work still required to close it.

It is against this backdrop of regional divergence that Thailand’s business sentiment has softened most noticeably. While neighbouring economies gathered momentum, Thailand’s mid-market entered 2026 operating under the combined weight of external shocks and unresolved domestic constraints;testing resilience across sectors.

Ian Pascoe, CEO & Managing Partner, Grant Thornton in Thailand, commented:

“Thailand’s mid-market is navigating one of the most demanding operating environments in recent memory. The war in Iran is the latest external shock, coming at a time when many businesses were already operating cautiously amid slower decision-making, delayed hiring and tighter spending controls.

This is less about businesses retreating entirely and more about a period of recalibration. Investment appetite remains, but decisions are increasingly selective focused on near-term value, productivity impact and operational resilience. The fundamentals that will determine Thailand’s competitiveness; technology adoption, talent development and execution discipline—cannot be deferred, even in a more subdued environment.”

Recalibration, Not Retreat

Thailand’s exposure to rising energy and logistics costs makes the current period particularly testing. Sourcing approximately 60% of its oil from the Middle East, Thailand faces above-average vulnerability within Asia as global energy routes remain disrupted. For an economy heavily dependent on exports and tourism, sustained pressure on supply chains represents a material risk to the 2026 outlook.

Yet across the mid-market, the response has largely been pragmatic rather than defensive. Business leaders are recalibrating;balancing short‑term caution with the recognition that structural investments cannot be postponed indefinitely without undermining long‑term competitiveness.

The war in Iran has added fresh disruption to an already fragile environment, driving up shipping costs, weighing on order books and reinforcing geopolitical uncertainty. These pressures come on top of longer-standing domestic challenges: a rapidly ageing population, tightening labour supply, high levels of household and corporate debt, and persistent productivity constraints.

Selective Investment and the Productivity Imperative

Despite softer confidence, Thailand’s mid-market is not standing still. Technology and digital investment remain active, though increasingly targeted. Rather than large-scale transformation programmes, many organisations are prioritising incremental productivity gains—using AI and digital tools to improve efficiency, support leaner operating models and deliver clearer near-term returns.

The opportunity now lies in execution. Converting Thailand’s strong foreign direct investment pipeline and growing technology agenda into tangible productivity improvements will be critical if the country is to narrow the gap with regional peers and sustain competitiveness over the medium term.

Chris, Chairman, Grant Thornton in Thailand, added:

“Periods of sustained uncertainty test not only economic resilience, but leadership effectiveness. What we are seeing across Thailand’s mid-market is a thoughtful recalibration;leaders balancing caution with clear-eyed investment decisions tied closely to value and execution.

The underlying pressures on businesses have not eased, even as confidence softens. The challenge now is to maintain momentum in capability building, organisational effectiveness and selective transformation, while operating with discipline and clarity in an uncertain external environment.”

About Grant Thornton in Thailand

Grant Thornton in Thailand is one of the world’s leading organisations of independent assurance, tax and advisory firms. Established in 1991, Grant Thornton combines global reach with deep local market expertise to support clients across diverse industries and help them capture growth opportunities.

For media inquiries, please contact:

Rattanakorn Sutthiphongkait

Marketing Communications and Branding Manager

Grant Thornton, Thailand

E: rattanakorn.sutthiphongkait@th.gt.com

W: grantthornton.co.th

Download a copy of International Business Report Q1 (2026)

Experts / Authors

-

Rattanakorn (KJ) Sutthiphongkait Marketing professional with 14+ years of experience in branding, digital marketing, and strategic communications. Currently Marketing Communications and Branding Manager at Grant Thornton Thailand, driving brand visibility and stakeholder engagement. Former Strategic Partnership Manager, leading value-driven collaborations and business growth.

Rattanakorn (KJ) Sutthiphongkait Marketing professional with 14+ years of experience in branding, digital marketing, and strategic communications. Currently Marketing Communications and Branding Manager at Grant Thornton Thailand, driving brand visibility and stakeholder engagement. Former Strategic Partnership Manager, leading value-driven collaborations and business growth.Let’s connect and explore opportunities to collaborate!