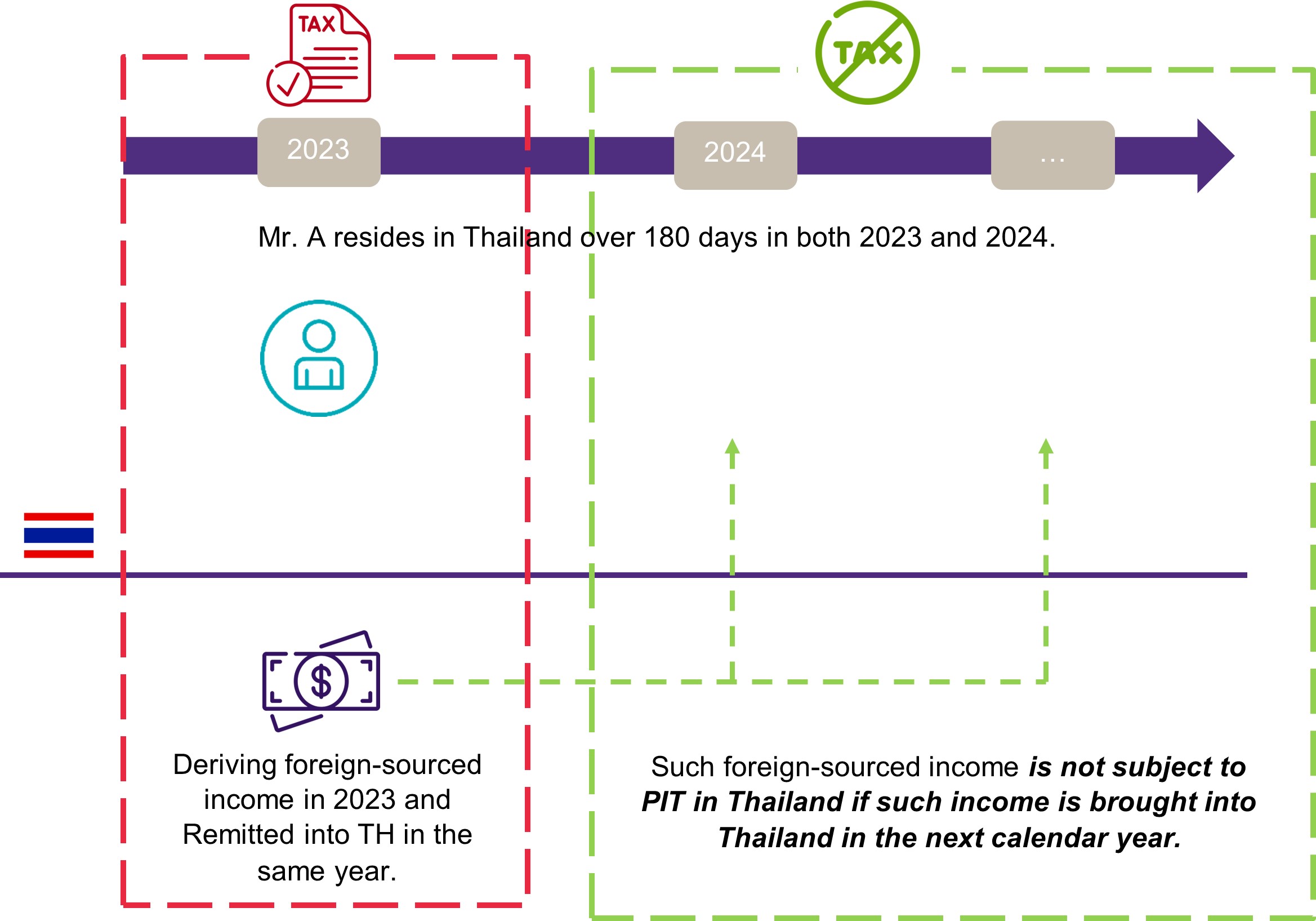

Prior Practice

Prior to this new departmental instruction, a Thai tax resident[1] is liable to income tax on foreign-sourced income if such income is remitted into Thailand in the same calendar year to which the income was earned. In other words, foreign-sourced income is not taxable if it is brought into Thailand in the subsequent calendar year.

Example

[1] A Thai tax resident refers to any person staying in Thailand for a period or periods aggregating 180 days in any tax year.

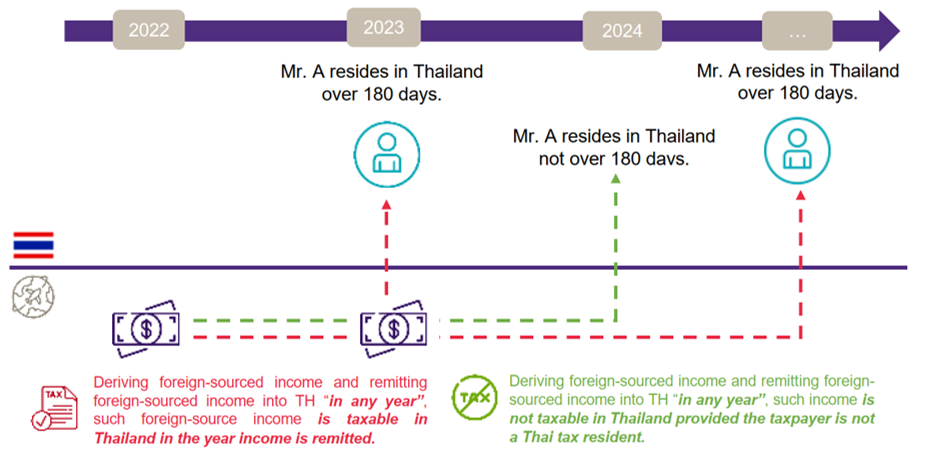

New Practice

Under the new department instruction, a Thai tax resident with foreign-sourced income will be taxed in Thailand when such foreign-sourced income is remitted into Thailand irrespective of when such income is remitted into Thailand.

Note that this rule applies only to Thai tax residents.

Example

Our view:

This new guideline presents significant challenges for Thai tax residents who have both Thai and foreign-sourced income. While the department instruction is not law, it represents the enforcement directive of the tax authority.

We find that the tax authority stills needs to further address several issues relating to how this new rule will be enforced. For instance, the applicable tax rates (whether there will be any flat tax imposed, different tax rates specifically applied for foreign-sourced income, or at the standard progressive tax rate), how to distinguish between principal (funds from legacy investments, inheritance, original investment principal) versus earnings (interest, dividends, renumeration) from comingled funds, determination of applicable foreign currency exchange rates for tax assessment, etc.

At the time of this writing, Grant Thornton is actively following up on further developments on this matter. We hope to provide further updates and clarifications on this topic in the near future.

About us:

Grant Thornton provides a range of corporate services and advisory, including audit and assurance, business consulting, business process outsourcing, business risk services, financial advisory, and tax advisory. Our tax advisory team is staffed by Thai and foreign tax specialists who advises clients in various capacities, including tax structuring and planning, tax dispute resolution, tax compliance, transfer pricing, and customs and excise taxes.