Transfer Pricing update and the New E-Services Tax

01 Mar 2021Thailand is revising its Country-by-Country Reporting (“CbCR”) regulations in ways that will significantly impact companies that do business within its borders. The following overview is intended to help entities understand how these changes may affect them moving forward.

Update on Country-by-Country Reporting (“CbCR”) Regulations

The Thai Revenue Department (“TRD”) has released a draft regulation on the CbCR filing, one tier of a three-tiered approach to transfer pricing documentation. The CbCR filing requirement covers the accounting period commencing on or after 1 January 2020.

CbCR is designed to gather information on global allocation of revenue, profit, and tax among jurisdictions that the members of Multinational Enterprises (“MNEs”) operate.[1] CbCR will then be exchanged among tax authorities of various jurisdictions through the system and will be used as a risk assessment tool.

Provided below are the important points of the draft CbCR regulation:

Entities required to file CbCR in Thailand: MNEs with a consolidated revenue of 28 billion Baht and above in the previous accounting period, and the associated enterprises of such MNEs, which fall under the following conditions:

General case

- The ultimate parent entity is incorporated under Thai laws; or

- The ultimate parent’s representative company is incorporated under Thai laws.

Specific case

- A company that does not fall under (1) and (2) but operates in Thailand and meets at least one of the following criteria:

- The tax jurisdiction of the ultimate parent does not require the filing of CbCR, and the ultimate parent does not appoint any representative to file CbCR; or

- The tax authorities of the jurisdiction where the ultimate parent or the representative of the ultimate parent is located did not enter into an international agreement stating that the counterparties are required to automatically exchange CbCR, or the agreement is not yet in effect; or

- If there is an existing international agreement but the TRD receives notification of system failure, or the exchange of CbCR is suspended, or the sending fails, from the tax jurisdiction of the ultimate parent or the representative of the ultimate parent.

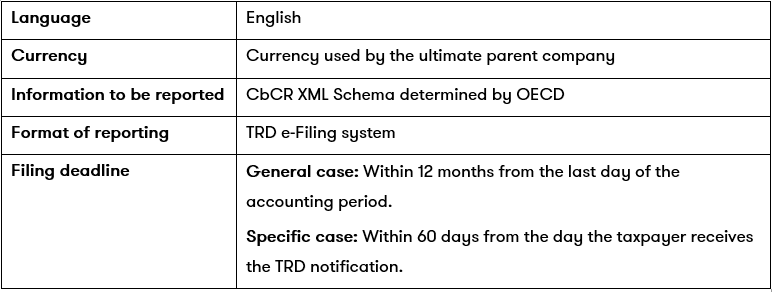

CbCR filing:

Notification on Transfer Pricing Methodologies

On 14 January 2021, the Thai Revenue Department (TRD) released the Director-General Notification No. 400 (Notification) on the Transfer Pricing (TP) methodologies. The Notification applies to accounting periods commencing on or after 1 January 2021. The benefits derived by a company from a related-party transaction must be at arm’s length. Otherwise, the assessment officer has the authority to adjust either the income or expense of both domestic and overseas related entities, which may cause the payment of additional taxes.

The function, assets, and risk (“FAR”) as well as other economic factors must be considered in the selection of the TP method. The benchmarking analysis must be conducted and updated on an annual basis.

Based on the nature of the business and information available, the most appropriate TP method must be selected for the benchmarking analysis. The five TP methods are: (i) Comparable Uncontrolled Price Method; (ii) Resale Price Method; (iii) Cost-Plus Method; (iv) Transactional Net Margin Method; and (v) Transactional Profit Split Method.

The Notification also states that for services, the parties must provide sufficient evidence of the service provided and the economical or commercial benefit derived from it. With regard to related party transactions on intangible assets, the same will be evaluated using the development, enhancement, maintenance, protection, and exploitation (DEMPE) analysis, together with the assets and risks borne by the relevant member of the MNEs.

Imposition of E-Services Tax

On 10 February 2021, the law amending the Thai Revenue Code on E-Services Tax was announced in the Royal Gazette. The majority of the relevant provisions of the law will be effective from 1 September 2021. The E-Services Tax will impose VAT to any foreign company providing e-services through an e-platform to a non-VAT registrant customer in Thailand.

E-Services and E-Platform, defined

The law defines “electronic service” as a service that includes intangible property delivered via the internet or any other electronic means, whereby for the most part, the service is automated and cannot be carried out without the use of information technology.

“electronic platform” means a market, channel or any processes that the provider uses in order to render the service.

Parties covered

Foreign companies:

- That provide electronic services or services through an electronic platform to a non-VAT registrant customer in Thailand; and

- With annual revenue of 1.8 million Baht or more.

Registration requirement

A foreign company that falls within the abovementioned conditions must register for VAT via the online system with the TRD. The foreign company must pay 7% output tax without the ability to credit any input tax. The VAT return must be lodged using the electronic filing method within 15 days of the following month.

In cases where services are provided through an electronic platform, the platform provider must pay the VAT on behalf of the electronic service provider. In such cases, the platform provider will have the same liability as the electronic service provider.

[1] Transfer Pricing Documentation and Country-by-Country Reporting, Action 13 – 2015 Final Report, para 24